‘Rebate gate’ (Part 2 of 2) – Potential Consequences

Will the real price be revealed?

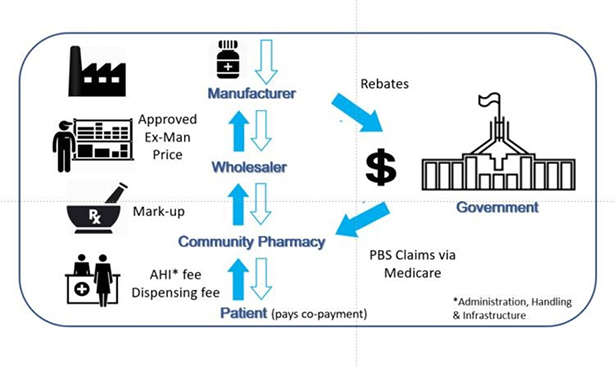

As described in Part 1, the Australian Federal Government wants to eliminate an existing process whereby certain PBS medicines are reimbursed through the supply chain at ‘published (list) prices’, even though a lower price, known as the ‘effective price’ has been agreed. At a latter date, sponsor companies repay (rebate) the difference between these two prices to the Government. For medicines where this applies, the real price paid is kept confidential for international reference pricing purposes, with the trade-off being subsidised access for Australian patients.

The schematic shows a simplified version of the current flow of money and product through the supply chain from manufacturer to patient based on the published price in the PBS schedule. Note that as mark-ups and fees are calculated on the published price, relevant adjustments are made and also repaid by sponsor companies as part of rebate amounts.

Who pays and when?

The Government is proposing that instead of one Medicare payment being made to a pharmacy on submission of an eligible claim for a dispensed PBS item, for those products to which a rebate applies, the Government will directly pay each step in the supply chain the relevant amount based on the effective price.

Two potential consequences become clear:

1. Loss of confidentiality of the ‘effective price’. This should be of concern, as it means Australia may be moved to the end of the list of countries provided with the registration dossier for a new medicine. This will add years to the wait for innovative medicines before the TGA or the PBAC even get to consider the value offered to the Australia public.

It is the perfect storm as local affiliates will be forced to sacrifice access for Australian patients for markets that reference to PBS prices. This is a very real phenomenon, and decisions not to launch, or withdraw products have already been made locally by companies due to international reference pricing concerns.

You don’t need to look far to appreciate what the future may look like.

2. Business mayhem. What happens to well-established terms of trade and legalities around ownership of goods and responsibility for product condition (cold chain continuance, breakages, delivery failures, etc.) with a move to agent status on the basis of ‘phantom’ invoices? The payment of GST as required at the various steps in the process will also need new systems and processes to ensure that obligations to the Australian Tax Office continue to be met (watch this week’s abc Four Corners program).

A way forward?

Without compromise, it is unlikely that change of such magnitude will be in place by the arbitrary time frame of 1 July 2018. Retaining the current arrangements with tweaks seems most sensible. What about tighter (such as, monthly) time frames around repayments to the Government? This would require a quicker turnaround of invoices than has currently been the case. Another option is for companies to pay rebates (monthly or quarterly) in advance based on Deed agreed utilisation estimates. Perhaps you have a better idea?